Moving real money in and out

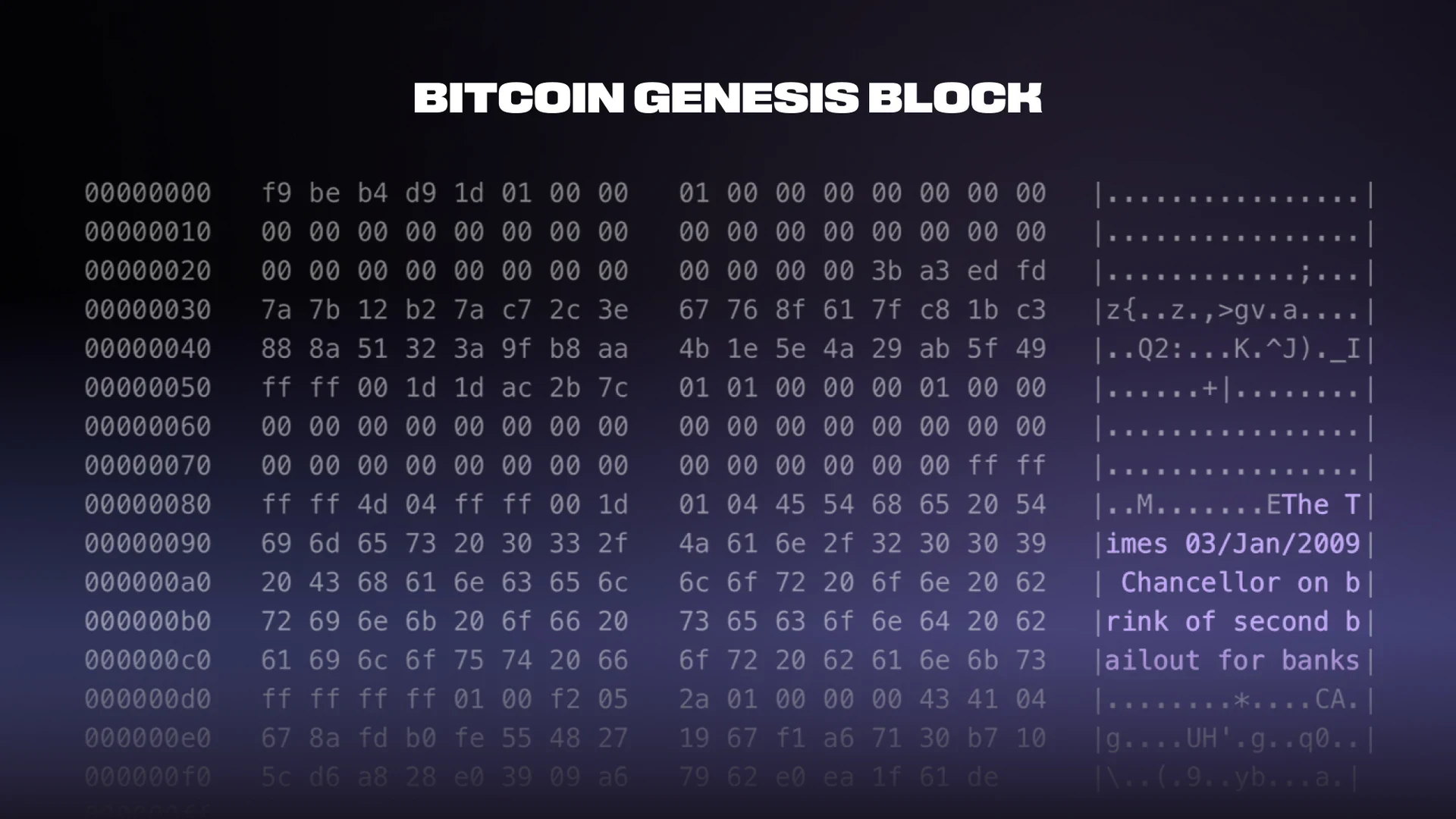

In January 2009, in the wreckage of the worst financial crisis in living memory, Satoshi mined the first block of Bitcoin and left a message inside it: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.” Bitcoin started with a single proposition: there had to be a way to hold value that did not depend on any government, or the solvency or goodwill of any institution.

That single block was the catalyst for everything that followed. What began as a cypherpunk experiment — a few thousand people who cared about cryptography and self-determination — grew into an industry measured in trillions. Today the largest asset managers on earth run spot Bitcoin ETFs, pension funds hold allocations, and the institutional infrastructure that once seemed impossible is simply assumed. Crypto went through one of the fastest institutionalizations of any asset class in history, and yet there is a strange lag in how the financial system treats it.

Regulators and governments look far less hostile than they did just a few years ago — in the United States, parts of the establishment are openly cheering the industry on. But walk into a bank, and the picture changes. Many compliance departments still regard crypto as a threat to be managed rather than a tool to be understood. The irony is hard to miss as the people whose job is to follow money and detect wrongdoing should be crypto’s greatest champions, because crypto is radically more transparent than the system they defend. Every transaction sits on a public ledger, permanent and auditable, available to anyone with the patience to look. Moving illicit money through crypto is harder, not easier, than moving it through the opaque correspondent-banking networks.

As blockchain analytics capabilities have matured, the use of major public cryptocurrencies for money laundering and other illicit activity has become increasingly risky. Firms such as Chainalysis, Elliptic, TRM Labs, and Crystal Blockchain now provide sophisticated tracing tools that enable law enforcement, regulators, and financial institutions to follow the movement of funds across public ledgers and identify links to criminal activity. This has made it far more difficult for criminals to convert illicit proceeds into fiat currency, as regulated exchanges routinely flag, freeze, or report suspicious transactions. While illicit activity involving cryptocurrencies still exists, its share of overall crypto transaction volume has declined significantly as legitimate adoption has expanded. Moreover, agencies including Europol and the Financial Action Task Force (FATF) continue to note that traditional money laundering remains overwhelmingly cash- and banking-based, reflecting the reality that public blockchains create a permanent and highly transparent transaction record. Rather than serving as ideal tools for concealment, major public cryptocurrencies have increasingly become valuable sources of evidence for investigators.

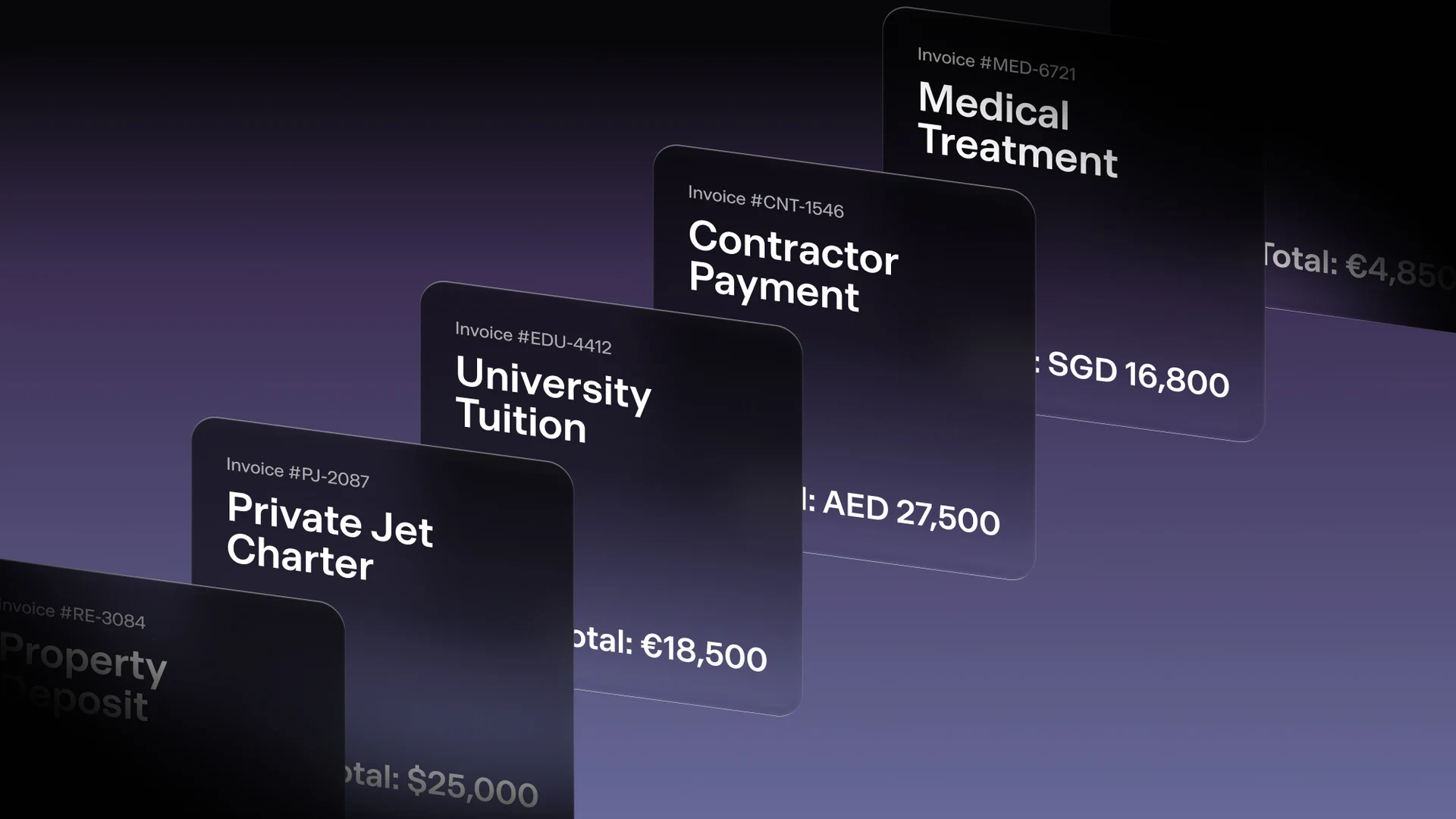

Whatever one thinks of that attitude, the practical need is undeniable: the world needs a clean bridge between crypto and fiat, and it needs one that works at scale. More and more wealth is flowing into the space every year, and the people creating that wealth eventually have to spend it in the physical world — where everything is still settled in fiat. Most of the solutions that exist today try to solve this with a card: you issue a debit card linked to your wallet and spend as you would with any other. That is useful for a coffee or a flight, but it is only a partial answer as you cannot, for example, buy a house with a debit card. You cannot move serious money — millions, not thousands — through a card rail. For anyone who needs to convert real size from crypto into fiat, that functionality simply has not existed.

When we built on- and off-ramp in Bron, we went back to first principles and designed for the use case that nobody else was serving. Three things mattered most to us:

First, you should be able to move between fiat and crypto in size. Not a few thousand dollars a day, but millions, in a single transaction, when you actually need to. The only thing that should ever limit you is your source of funds — the basic, legitimate question of whether the money is yours and where it came from. If it is yours and it came from a legitimate source, you should be able to move it. Everything else is friction that exists only because the rails were never built for people operating at this level.

Second, we designed around the reality that many banks remain crypto-hostile, and that being right or wrong about that is beside the point. A compliance department that sees anything crypto-related can freeze or close an account with little warning, leaving you to untangle the consequences. To protect you from that, the product works through our licensed partner, using a named bank account opened in your own name. You are not sending money to a stranger or receiving it from an exchange; you are moving funds between your own accounts. That structure spares you the uncomfortable questions and the sudden account closures, because to the banking system it looks like exactly what it is — your money, moving between accounts you own.

Third, we made sure you can pay the bills of a real life. Crypto is one of the best cross-border payment technologies ever invented, and it should let you settle obligations in the currencies those are denominated in. If your children study abroad, you should be able to pay their tuition. If you are hiring a jet or settling an invoice with a supplier on another continent, you should be able to do that too. Our licensed partner, noah.com, supports third-party payments and payouts in over a hundred currencies worldwide — so the off-ramp is not just a way to cash out, it is a way to pay.

There is a deeper reason all of this matters, and it has to do with the kind of world we now live in. We live in an age of compounding uncertainty, and the higher you climb the wealth ladder, the more exposed to that uncertainty you become. The geopolitical map is more polarized and less predictable than it has been in decades. In that environment, holding a portion of your wealth in self-custodial form becomes simply rational. And here crypto is superior to gold or property in one decisive respect: it moves with you easily. If you ever need to change where you live, you cannot fold a vault of gold into your pocket, but you can carry your crypto across any border in your phone or laptop.

But perhaps you read all of this and think: that kind of turbulence is not for me. I live in a stable, well-established country, and nothing like that could ever reach me. Even then, self-custody still matters, because life is full of events no one can forecast: a commercial dispute, a falling-out with a partner, or — God forbid — a divorce. What tends to happen in those moments is that your assets sitting in banks get frozen, often for years, while you are still expected to pay your lawyers and keep your life running. Holding part of your wealth outside the custodial system is what lets you do that. It is one thing to ask a friend to cover a bill and repay them in crypto right after. It is something else entirely to ask them to settle a lawyer’s invoice on the promise that you will pay them back when the case is finally resolved — which might be years away, if ever.

This is why on- and off-ramp functionality that works at real scale is so important. It lets you move a portion of your wealth into crypto in a fully transparent, fully compliant way, with every supporting document in order — and it is designed so that you can move it back into fiat when you need that money in the real world. That is not only a hedge against the system, but a rational way to live inside it. And for the first time, there is a solution built to do exactly that.

That is what we built into Bron: rails, operated by our licensed partners, that move your wealth in and out — safely, compliantly, and at scale — so you no longer have to think about it. Bron takes care of protecting what you have built while you get on with what actually matters to you.

Disclaimer:

This article is provided for general informational purposes only and does not constitute financial, investment, accounting, tax, or legal advice.

Bron is a self-custodial software wallet. Bron does not take custody of, hold, control, or access user assets or private keys, and does not provide exchange, transfer, payment, money-transmission, brokerage, or custodial services. Any on-ramp, off-ramp or payment functionality referenced above is provided by independent, separately regulated third parties; Bron is not a party to, and does not intermediate, arrange, match, route, or execute, those transactions. Eligibility, onboarding, source-of-funds verification, KYC/AML checks, and any transaction limits are determined and applied by those third parties, not by Bron. Availability of on- and off-ramp functionality may be restricted by jurisdiction, and nothing here is an offer, inducement, or invitation to engage in any investment or financial activity.

While Bron’s architecture is designed to eliminate single points of failure and reduce certain risks, the use of blockchain technology and self-custodial wallets involves inherent operational, technical, governance, and security risks, including those related to user configuration, device compromise, social engineering, or software vulnerabilities. Users remain solely responsible for evaluating their own circumstances, security practices, and risk tolerance.