Real Yield: Why Crypto Staking Delivers What Government Bonds Can't

A Basket of Beef, Corn, Wool, and Leather

1780, the middle of the American Revolutionary War, soldiers fighting for the Commonwealth of Massachusetts faced a problem that had nothing to do with the British. Their wages, paid in Continental currency, were evaporating. Wartime inflation had made the money nearly worthless by the time soldiers received it. If you ever heard “not worth a Continental”, this saying is the reference to that currency. It lost over 99% of its value.

To fight this problem, the Massachusetts legislature issued bonds whose value was tied not to a fixed amount of currency, but to the market prices of four essential commodities: corn, beef, wool, and leather weighted in certain proportions. If those prices rose, the bondholder’s payout rose with them. The soldiers, being paid in bonds, were, in effect, being promised real purchasing power rather than nominal currency.

These Massachusetts “depreciation notes” were the world’s first known inflation-indexed bonds. And then, the moment the immediate crisis passed, the concept was abandoned and largely forgotten.

Two Centuries Later

It wasn’t until 1955 that a government revisited the concept. Israel, battling severe inflation in the years following its founding, began issuing inflation-linked government bonds — initially restricted to pension funds and insurance companies. Israel had no choice: the inflation was so persistent that no one would buy fixed-rate government debt.

The United Kingdom followed in 1981, issuing its first index-linked GILT. Britain was fighting double-digit inflation, and the Government’s message was effectively: we are putting our money where our mouth is. If inflation does not come down, we will pay you more. The GILT was initially restricted to pension funds — a pattern that would repeat with every innovation in this space, where institutions get access to cool products first and everyone else waits.

The United States, despite being the world’s largest bond market, did not issue Treasury Inflation-Protected Securities — TIPS — until January 1997. For over two hundred years, the most sophisticated capital market on the planet offered no instrument that protected savers from the erosion of their purchasing power.

The Problem with “Inflation Protection”

Although the idea is great on paper, there is a fundamental issue with every government inflation-protected bond: the yield is linked to an inflation rate that the government itself calculates. TIPS are indexed to the Consumer Price Index. UK GILTS are indexed to the Retail Price Index. The entity that pays you more when inflation rises also controls the entity that measures inflation.

Over the past several decades, the methodology behind CPI has been revised repeatedly. Hedonic adjustments allow statistical agencies to reduce the recorded price of goods by claiming that quality improvements offset price increases — your laptop costs more, but it is a better laptop, so the price increase does not fully count. Substitution effects allow the basket to shift: if beef becomes expensive, the model assumes consumers switch to chicken, and the index reflects the cheaper option. Geometric weighting further reduces measured inflation compared to older arithmetic methods.

The cumulative effect is significant. Depending on which methodology you use, the rate of inflation in the United States over the past two decades diverges dramatically. The official CPI consistently shows lower inflation than methodologies that use the pre-1990 approach. The gap is not trivial — it can be several percentage points per year, compounding into a vast difference over time. For anyone holding TIPS and believing they are fully protected against purchasing-power erosion, this is an uncomfortable truth: the “inflation” you are being compensated for may be substantially lower than the inflation you experience visiting a supermarket.

Crypto Staking: Yield You Can Verify

This is where crypto staking offers something genuinely different. In proof-of-stake networks like Ethereum and Solana, staking rewards are not linked to any government-defined index. They are protocol-level issuance — new tokens distributed to validators who secure the network. And critically, the “inflation” of the token supply is also determined by the protocol, transparently, on-chain, and impossible to manipulate after the fact.

This means you can calculate real yield precisely and independent of a statistical agency of any government.

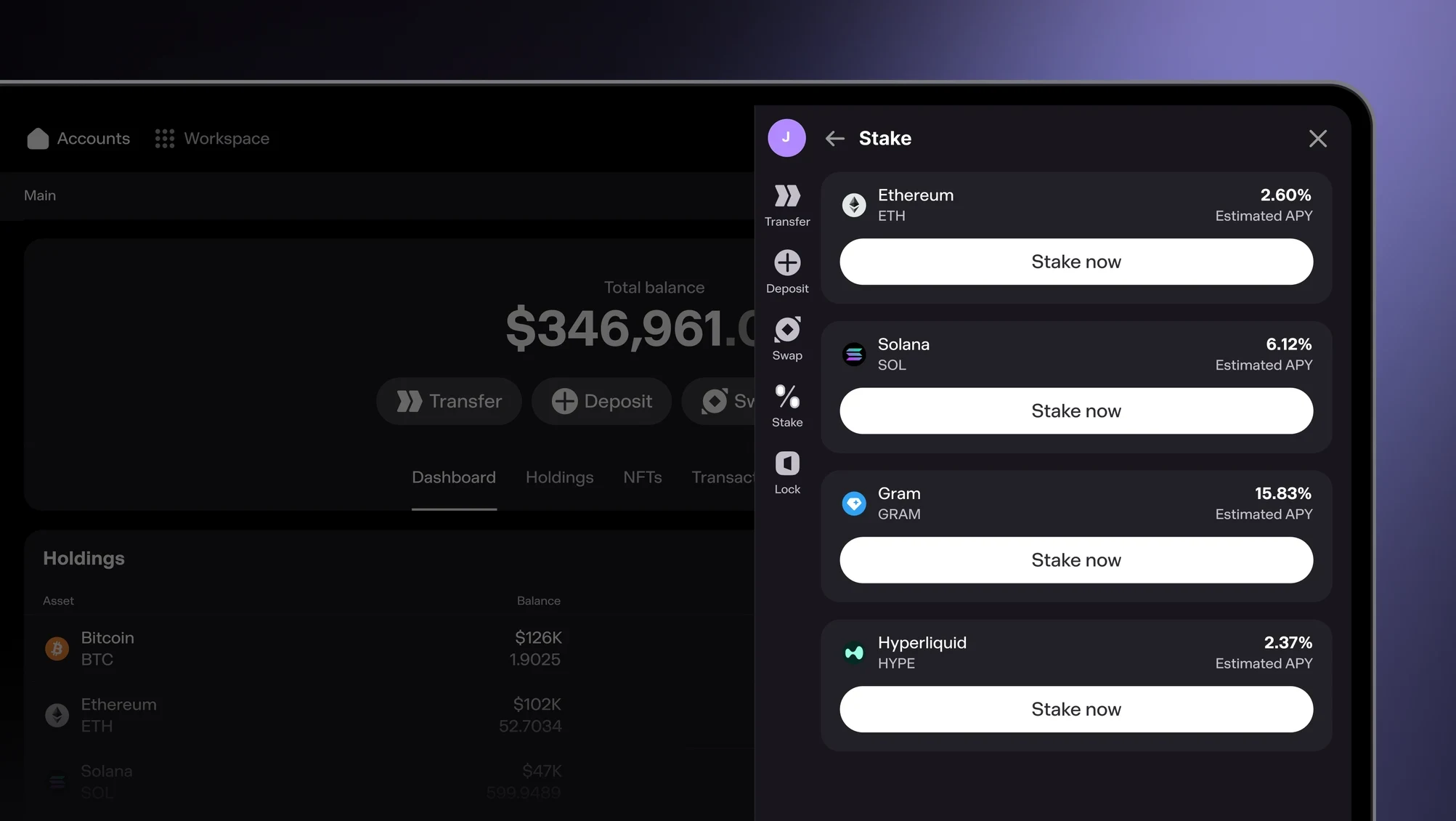

Ethereum

Currently offers a staking yield of approximately 2.8–3.0% per annum. The network’s net inflation rate — new issuance minus tokens burned through the EIP-1559 fee mechanism — sits at roughly 0.7% annualised. The real yield to stakers is therefore approximately 2–2.5%, and every component of that calculation is publicly verifiable on-chain.

Solana

Operates with a higher inflation rate — currently around 4.6% and declining on a fixed disinflationary schedule toward 1.5% — but staking yields of 6–7.5% more than compensate. With approximately 68% of circulating SOL staked, validators earn a meaningful real return even after accounting for new supply. The protocol’s economics are transparent, predictable, and not subject to retroactive revision.

Hyperliquid

Takes this further. The HYPE token offers staking yields of approximately 2.3%, but the protocol directs 97% of its trading fees into daily buybacks and burns of HYPE tokens. The result is that Hyperliquid is actively deflationary — the circulating supply is shrinking. Staking HYPE means earning yield on an asset whose supply is contracting, a dynamic that no government bond has ever offered.

Back to Basics

The Massachusetts soldiers in 1780 wanted something simple: to be paid in a way that preserved their purchasing power. The concept they were given was elegant, effective, and… promptly forgotten.

When governments eventually rediscovered the idea, they anchored it to indices they controlled. The result is an instrument that offers the appearance of inflation protection while leaving the definition of inflation in the hands of the issuer. It is better than nothing, but it is not the transparent, verifiable protection that the Massachusetts model originally envisioned.

Crypto staking is closer to what those Revolutionary War bonds were trying to achieve than TIPS or index-linked GILTS are. The yield is real. The inflation is measurable. Neither is subject to retroactive manipulation. You do not need to trust a statistical agency to calculate your return honestly — you can verify it yourself, on-chain, at any time.

Stake with Confidence

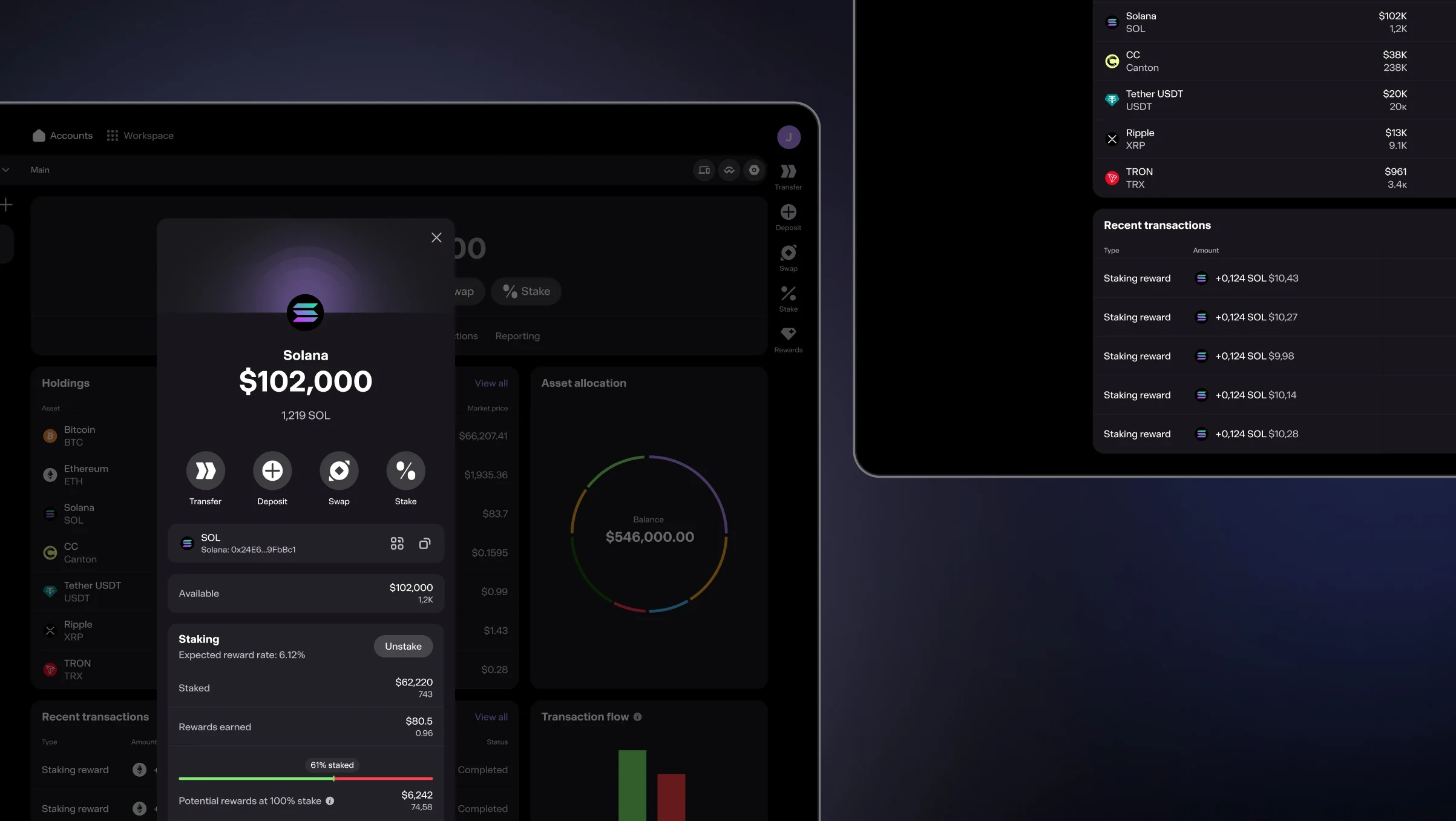

At Bron, we believe that participating in proof-of-stake networks should be as simple and secure as self-custody. That is why you can connect to validator infrastructure directly from the Bron wallet through an integration with P2P.org — one of the world’s leading non-custodial staking providers, with billions of dollars in delegated assets. P2P.org operates validators independently of Bron, and tokens stay in your self-custody throughout.

Staking through the Bron wallet takes a single tap. Select the asset, sign the transaction with your device, and your tokens are delegated to a P2P.org validator without ever leaving your wallet. Any rewards are issued directly by the underlying network. There is no need to manage validators, run infrastructure, or navigate complex interfaces. Your assets remain non-custodial throughout — secured by Bron’s MPC architecture, where no single party, including Bron, can access your funds. The same institutional-grade security that protects your holdings also protects your staking positions.

Whether you are staking Ethereum, Solana, Gram or HYPE, any rewards are determined transparently on-chain and are subject to protocol economics that may change. Rewards are not guaranteed and are not set by Bron.

Two hundred years after those first depreciation notes were issued, the concept has finally found a medium worthy of it. And with Bron, it is available to you at the tap of a button.

Important:

Rewards from proof-of-stake networks are not guaranteed and are determined by the underlying protocols, which may change. Staking availability is subject to local laws and regulations in your jurisdiction. Nothing in this article constitutes financial, legal, or investment advice.